Response to Comptroller Opposition: Fair Tax Act

Response to the Ulster County Comptroller’s Opposition to the Ulster County Fair Taxes Act

Resolution No. 2026-295 Prepared by Majority Leader Abe Uchitelle, Ulster County Legislature | June 2026

Introduction

On June 9, 2026, Ulster County Comptroller March S. Gallagher published a blog post raising four concerns about the Ulster County Fair Taxes Act (Resolution No. 2026-295). The Comptroller’s engagement with the proposal is welcome. Indeed, the Comptroller herself acknowledges that new revenues may be necessary, writing that she “applaud[s] the Executive and the Legislature for considering additional new revenue sources” and that “we may need additional revenues in the 2027 and 2028 budgets or else we could see property tax increases.”

Despite this acknowledgement, Comptroller Gallagher goes on to provide four criticisms. This memorandum addresses each in turn, drawing on county data, regional migration research, and the National Association of Counties’ (NACo) analysis of the federal cost shift now underway.

The Ulster County Fair Taxes Act would impose a modest surcharge on the highest-earning residents of Ulster County — those with individual taxable income above $200,000 or joint filers above $400,000. Ulster County’s median household income is approximately $84,000 per year — more than 75% less than the threshold proposed for joint filers. The county has not raised property taxes since 2012, a 31% real reduction when adjusted for inflation. The Fair Taxes Act is one of the few tools available to Ulster County to raise revenues progressively while protecting working families from regressive tax increases.

Concern 1: The Threshold Captures “Upper Middle Class” Households

The Comptroller’s Claim

The Comptroller argues that the surcharge thresholds capture not just the “top 1%” of Ulster County residents but rather the “top 3.3–3.8% of filers.” She contends that “the wedge should be driven between nearly all of us and the billionaire class,” implying the threshold is set too low.

Response

The Comptroller’s framing is misleading. Only 2.4% of Ulster County households would be affected by the surcharge, and the surcharge represents less than 1% of total income for those affected filers. As County Executive Jen Metzger noted, “the median household income in Ulster County is less than a quarter of that” $400,000 threshold. A household earning the county’s median income could quadruple their earnings before paying a single dollar under the Fair Taxes Act.

And because the thresholds apply to New York taxable income (after deductions), a single filer needs gross income of approximately $231,000 before owing a single dollar under the surcharge. A joint filer needs approximately $451,000 in gross income. The effective entry point is significantly higher than the statutory threshold alone suggests.

Calling that threshold a sweep of the “moderately well off” is not a serious description of who these households are.

The Comptroller’s own analysis concedes that households in the $200,000 to $249,000 range would generate only “trivial” revenues. She agrees, in other words, that the overwhelming majority of revenue would come from the highest earners. Her objection that the threshold is too low is thus in tension with her own data: the proposal functions as she says a tax like this should, concentrating the burden at the top.

This argument may come down to what one considers to be “middle class.” Under the current proposal, it is projected that 97% of Ulster County households would not pay any additional taxes. We encourage the public to visit ucfairtax.com to explore projections of additional estimated taxes based on their taxable income.

Concern 2: The Surcharge May Drive Outmigration

The Comptroller’s Claim

The Comptroller acknowledges that “[t]here is a split in the literature about whether tax increases actually do cause outmigration,” but nonetheless suggests that the surcharge thresholds “may dissuade certain professionals from making residence in Ulster County.” Her primary example is physician recruitment: “we have a hard time recruiting doctors to Ulster County. This legislation will not help.”

Response

The Comptroller’s outmigration concern is directly contradicted by the most current data available. Hudson Valley Pattern for Progress analyzed IRS migration data released on March 25, 2026, covering 2021 and 2022. Their finding is unambiguous: Ulster County was the only county in the entire nine-county Hudson Valley region to gain population from migration — a net gain of 279 residents. Every other county lost people. The region as a whole experienced a net loss of 10,174 residents.

Ulster County also gained more net income from migration than any other county in the region — $169.2 million in new adjusted gross incomes. The households moving into Ulster County had significantly higher average incomes ($113,328) than those moving out ($79,598). Higher-income households are choosing Ulster County, and lower-income households who would be unaffected by this proposal are the ones being forced out.

The Pattern for Progress report also identifies what actually drives outmigration. For households leaving to neighboring states (Connecticut, Massachusetts, New Jersey, Pennsylvania), the dominant driver is property taxes, not income taxes; those movers save approximately 30–60% on property, income, and sales taxes combined. For households leaving to Florida, North Carolina, Texas, and similar southern states, the driver is retirement income exemptions that Ulster County could not replicate regardless of this proposed income surcharge policy.

The Fair Taxes Act is designed to generate revenues that can, among other uses, reduce pressure on property taxes — the very factor Pattern for Progress identifies as the primary cause of cross-border flight.

The Comptroller’s specific example — physician recruitment — deserves a direct answer. A physician earning $350,000 in Ulster County and filing as single would face a surcharge of roughly $1,500 to $2,000 per year. The suggestion that this amount would cause a doctor to choose against practicing in a county with Ulster’s quality of life, proximity to New York City, and demonstrably successful track record of attracting high-income residents is not grounded in the evidence.

Concern 3: The Proposal Is Being Considered in a Vacuum

The Comptroller’s Claim

The Comptroller argues that the Fair Taxes Act is being considered without adequate budgetary context. She writes that “there really haven’t been discussions in the budgetary context of cuts in light of the potential changes in federal funding which could increase Ulster County taxpayer responsibility for SNAP and Medicaid costs.” She suggests the Legislature should examine spending reductions and alternative revenues, including a real estate transfer tax, before or alongside an income surcharge.

Response

The premise of this concern is backwards. The federal fiscal picture is not speculative nor abstract and is the reason the Legislature is acting now. H.R. 1 (the “One Big Beautiful Bill Act”) has been enacted and its consequences are quantified and severe. According to analysis from the National Association of Counties:

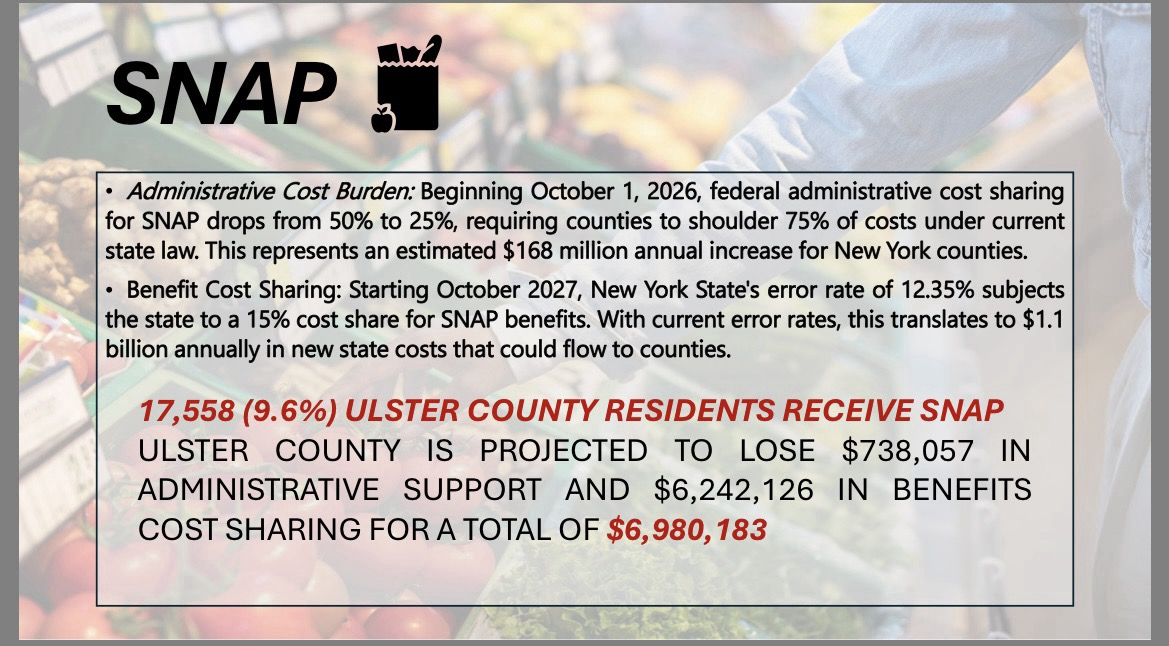

- Federal cost share for SNAP administration will fall from 50% to 25% starting in FY2027.

- New York counties could face up to $266 million in new annual SNAP administrative costs.

- Counties in New York already contribute up to $7.6 billion annually to the non-federal share of Medicaid.

- New benefit cost-sharing requirements tied to payment error rates will further increase county obligations.

- Nationally, NACo projects that federal cost shifts will produce a downstream effect approaching $1 trillion over ten years.

In fact, in a 2025 presentation the Comptroller herself estimated that the loss of SNAP administrative support and cost sharing benefits would reach almost $7M. Inflation and other economic metrics have increased in 2026, meaning this estimation is potentially low.

Source: Comptroller Gallagher’s Denning Town Hall on Federal Funds — July 29, 2025

The Comptroller’s blog post specifically cites increased SNAP and Medicaid exposure as the budgetary threat she is most concerned about. She is right to be concerned. But it is not the Legislature acting in a vacuum — it is the Legislature acting directly in response to a concrete, quantified threat that the Comptroller herself has named. The Fair Taxes Act is not being developed without a broader discussion; it is the broader discussion, translated into a specific progressive revenue tool.

The Comptroller’s suggestion to examine a real estate transfer tax alongside the Fair Taxes Act is worth taking seriously — yet this proposed alternative fails the very test the Comptroller herself proposes in her earlier criticism regarding who the tax would target. A transfer tax aimed at the top 25% of home sales would need a threshold somewhere between $575,000 and $650,000 based on current Ulster County price distributions. At that level, it would still fall on buyers who are stretching to purchase a home in one of the most difficult mortgage environments in decades. And if the threshold were set lower, at or near the median home price of $440,000, it would hit 50% of all transactions, including first-time buyers and growing families at the closing table. In comparison, the Fair Taxes Act only targets the wealthiest 2.5%.

The Legislature should also be clear about what “waiting for a comprehensive review” actually means in this context. The Fair Taxes Act requires state legislative approval and cannot take effect before 2027 at the earliest. To delay beyond that is not a responsible posture when the federal costs are already in motion, with their full scope being realized in 2028. And county governments cannot cut their way to solvency here. SNAP and Medicaid are mandated services. NACo is explicit: counties delivering these services cannot simply reduce them when federal funding is cut. They must absorb costs, raise local taxes, or allow services to degrade.

The Fair Taxes Act creates a progressive mechanism to fund these obligations without burdening working families through property tax increases or regressive sales taxes. It is essential that Ulster County is ahead of the curve in solving this state-wide budgeting problem.

Concern 4: The Proposal Lacks Financial Triggers and a Sunset Provision

The Comptroller’s Claim

The Comptroller argues that “the proposed law is not contingent on certain financial outcomes” and that the county resolution has not included discussion of a sunset provision or regular reauthorization, even though the enabling state legislation (A11460/S10532) permits localities to add one.

Response

No Ulster County tax is contingent on financial outcomes in the mechanical way she envisions. Holding the Fair Taxes Act to a different standard than every other revenue mechanism is not a principled objection; it is a higher bar applied selectively when only the highest earning residents will be affected.

Tying the surcharge to a strict fiscal trigger carries its own risks. The federal cost shifts NACo identifies will materialize through multiple mechanisms over several years: SNAP administrative costs, Medicaid share obligations, reductions in community development and public health funding. Designing a single trigger that accurately captures this multi-dimensional risk is technically complex and could leave the county unable to activate the surcharge during exactly the period of maximum need.

Conclusion

The Comptroller’s concerns, examined carefully, do not undermine the case for the Fair Taxes Act. They sharpen it.

The surcharge targets households earning more than four times the county’s median income. The most current regional migration data show Ulster County in a position of strength in the Hudson Valley, and the outmigration fear is directly contradicted by the available evidence. The federal fiscal environment is not speculative. H.R. 1 will shift up to $266 million in new SNAP administrative costs onto New York counties alone. Medicaid obligations are rising. A downstream county cost burden approaching $1 trillion nationally is already in motion.

In the years ahead, communities across New York and beyond will be struggling to carry the burden of the federal tax cuts. Putting this plan into motion now, with state passage in 2026, will ensure that we are prepared to carry that burden.

The Comptroller’s concerns about threshold indexing, accountability mechanisms, and broader fiscal strategy all deserve continued dialogue, and the Legislature welcomes that conversation. But they are refinements to a proposal that is well-founded in law, in data, and in the fiscal realities Ulster County faces. The Fair Taxes Act deserves passage.